[ad_1]

After we’re researching an organization, it is generally exhausting to seek out the warning indicators, however there are some monetary metrics that may assist spot bother early. A enterprise that is doubtlessly in decline typically reveals two traits, a return on capital employed (ROCE) that is declining, and a base of capital employed that is additionally declining. This reveals that the corporate is not compounding shareholder wealth as a result of returns are falling and its internet asset base is shrinking. In mild of that, from a primary look at Zhejiang Chang’an Renheng Expertise (HKG:8139), we have noticed some indicators that it could possibly be struggling, so let’s examine.

Understanding Return On Capital Employed (ROCE)

For those who aren’t certain what ROCE is, it measures the quantity of pre-tax earnings an organization can generate from the capital employed in its enterprise. The method for this calculation on Zhejiang Chang’an Renheng Expertise is:

Return on Capital Employed = Earnings Earlier than Curiosity and Tax (EBIT) ÷ (Complete Belongings – Present Liabilities)

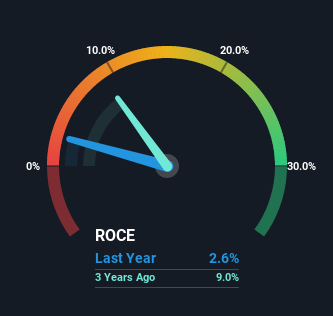

0.026 = CN¥3.0m ÷ (CN¥279m – CN¥164m) (Based mostly on the trailing twelve months to September 2022).

So, Zhejiang Chang’an Renheng Expertise has an ROCE of two.6%. In the end, that is a low return and it under-performs the Chemical compounds business common of 15%.

Check out our latest analysis for Zhejiang Chang’an Renheng Technology

Historic efficiency is a superb place to begin when researching a inventory so above you possibly can see the gauge for Zhejiang Chang’an Renheng Expertise’s ROCE in opposition to it is prior returns. If you wish to delve into the historic earnings, income and money circulation of Zhejiang Chang’an Renheng Expertise, try these free graphs here.

What Can We Inform From Zhejiang Chang’an Renheng Expertise’s ROCE Development?

We’re a bit nervous in regards to the development of returns on capital at Zhejiang Chang’an Renheng Expertise. To be extra particular, the ROCE was 5.0% 5 years in the past, however since then it has dropped noticeably. On prime of that, it is value noting that the quantity of capital employed throughout the enterprise has remained comparatively regular. This mixture will be indicative of a mature enterprise that also has areas to deploy capital, however the returns obtained aren’t as excessive due doubtlessly to new competitors or smaller margins. If these traits proceed, we would not count on Zhejiang Chang’an Renheng Expertise to show right into a multi-bagger.

On a facet be aware, Zhejiang Chang’an Renheng Expertise’s present liabilities have elevated over the past 5 years to 59% of complete property, successfully distorting the ROCE to some extent. If present liabilities hadn’t elevated as a lot as they did, the ROCE might truly be even decrease. What this implies is that in actuality, a somewhat giant portion of the enterprise is being funded by the likes of the corporate’s suppliers or short-term collectors, which might deliver some dangers of its personal.

What We Can Study From Zhejiang Chang’an Renheng Expertise’s ROCE

Ultimately, the development of decrease returns on the identical quantity of capital is not usually a sign that we’re a progress inventory. Traders have not taken kindly to those developments, because the inventory has declined 70% from the place it was 5 years in the past. With underlying traits that are not nice in these areas, we might think about trying elsewhere.

If you wish to proceed researching Zhejiang Chang’an Renheng Expertise, you could be to know in regards to the 2 warning signs that our evaluation has found.

Whereas Zhejiang Chang’an Renheng Expertise is not incomes the very best return, try this free list of companies that are earning high returns on equity with solid balance sheets.

Valuation is advanced, however we’re serving to make it easy.

Discover out whether or not Zhejiang Chang’an Renheng Expertise is doubtlessly over or undervalued by testing our complete evaluation, which incorporates honest worth estimates, dangers and warnings, dividends, insider transactions and monetary well being.

Have suggestions on this text? Involved in regards to the content material? Get in touch with us immediately. Alternatively, e-mail editorial-team (at) simplywallst.com.

This text by Merely Wall St is normal in nature. We offer commentary based mostly on historic information and analyst forecasts solely utilizing an unbiased methodology and our articles aren’t meant to be monetary recommendation. It doesn’t represent a suggestion to purchase or promote any inventory, and doesn’t take account of your aims, or your monetary scenario. We purpose to deliver you long-term targeted evaluation pushed by elementary information. Word that our evaluation could not issue within the newest price-sensitive firm bulletins or qualitative materials. Merely Wall St has no place in any shares talked about.

[ad_2]

Source link