[ad_1]

ktsimage

KULR Know-how Group (NYSE:KULR) has emerged as a pacesetter in specialised battery thermal and security administration. The merchandise right here embody thermal elements and software program instruments which can be essential to securing and monitoring lithium-ion batteries that are acknowledged as probably explosive in sure circumstances. The attraction right here is the numerous market alternative throughout functions in electrical automobiles, vitality storage techniques, and industrial gear that require these kind of options.

The corporate is ramping up a commercialization technique with its credibility backed by contracts with main companies and is even trusted by NASA which has used KULR options on the Worldwide Area Station. Whereas the inventory is high-risk contemplating recurring losses and adverse money flows, we spotlight an expectation for accelerating progress into 2023 supporting a extra constructive long-term outlook.

supply: firm IR

What Does KULR Do?

KULR is focusing on the rising demand for high-performance batteries and digital techniques that may run cooler, lighter, and safer. KULR’s thermal administration options lengthen throughout the whole life cycle of lithium-ion batteries and associated electronics.

The thought right here is that firms can incorporate KULR’s “Thermal Runaway Protect” and “Passive Propagation Resistant” options into the preliminary design and testing stage of latest battery merchandise. The use cases prolonged into safe transportation and recycling. Among the sensible benefits embody the light-weight and low-contact stress necessities in comparison with different options.

The income mannequin captures design providers, product gross sales, IP licensing, in addition to subscription alternatives that are all anticipated to be expanded sooner or later. We talked about NASA however different high-profile clients embody Protection and Aerospace leaders like Lockheed Martin Corp (LMT) and Raytheon Applied sciences Corp (RTX), and Airbus SE (OTCPK:EADSF).

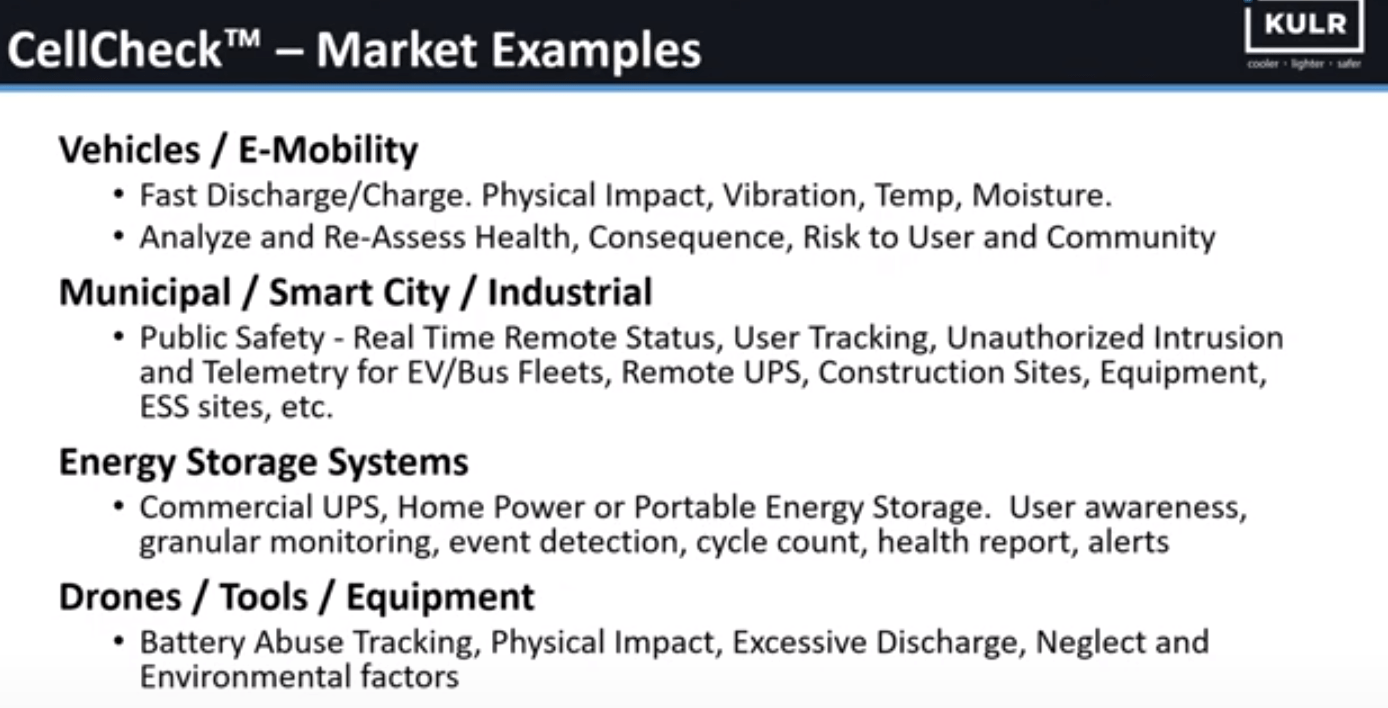

A featured product is the “CellCheck” battery administration platform which includes real-time monitoring of key efficiency and security indicators throughout temperature, moisture, discharge fee, and extra linked to a software program platform. The worth proposition right here for purchasers is to supply the world’s “smartest battery” with built-in security options. The current business launch is anticipated to a be a growth driver within the coming quarters.

supply: firm IR

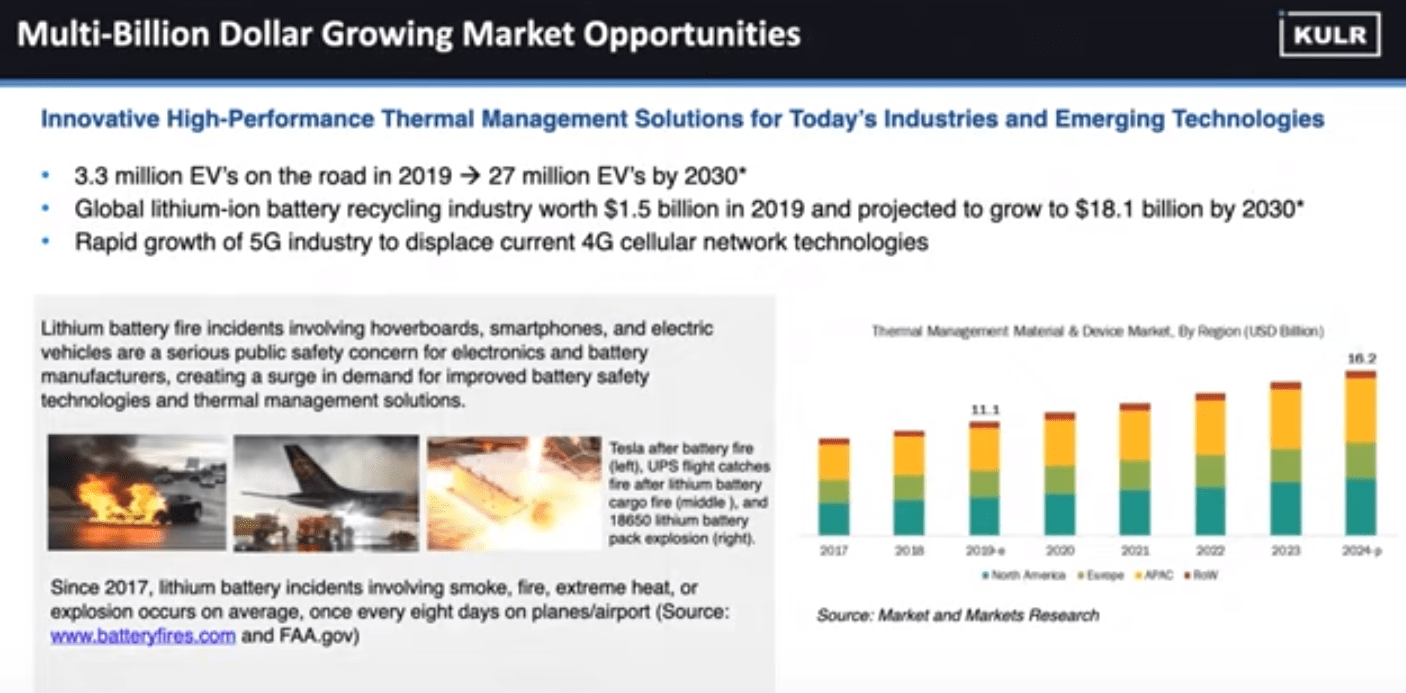

KULR administration sees a multi-billion greenback market alternative with the worldwide gross sales of thermal administration supplies climbing from $11.1 billion in 2019 to $16.2 billion by 2024. All the pieces from the expansion of electrical automobiles to lithium-ion recycling which requires protected transportation can profit from KULR options. Simply capturing an incremental slice of this chance represents the bullish case for the inventory.

supply: firm IR

KULR Key Metrics

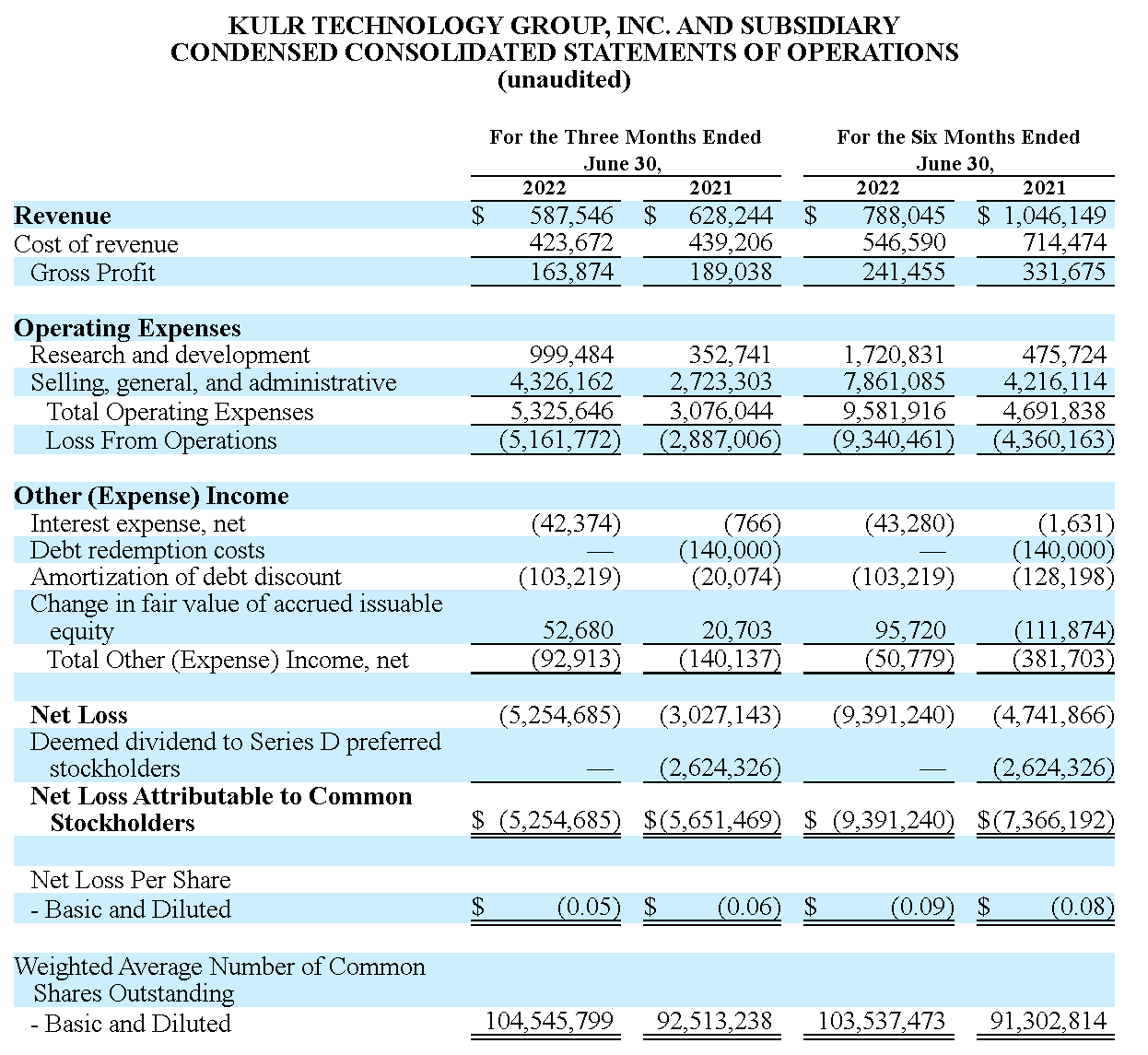

The corporate final reported its Q2 financials in August with $588k in income which was a decline in comparison with $628k within the quarter final yr. That being mentioned, the context right here is the timing within the rollout of latest merchandise and the lag in recognition of some massive orders. The ramp-up effort within the enterprise is clear by SG&A climbing by 59% year-over-year which features a push with advertising and an expanded gross sales pressure.

Total, the working loss yr so far has reached -$9.3 million though the corporate reported ending the quarter with $13 million in money. With adverse money flows anticipated to proceed for the foreseeable future, the technique can be to boost capital by way of further fairness issuances. After the quarter’s finish, KULR has introduced upwards of $50 million in standby fairness buy agreements, which administration believes go away the corporate positioned to broaden the enterprise and scale appropriately.

supply: firm IR

There’s little to cherry-pick by way of the financials which can be objectively weak. That being mentioned, a number of developments in current months preserve the inventory fascinating. The primary level here’s a sequence of headlines with new contract bulletins. In September KULR obtained approval from the Division of Transportation to extend the vitality degree shipment certification for its “SafeCase” product as much as 2.5 kWh batteries. This opens up new business alternatives for large-scale deployments requiring this sort of certification for finish customers.

Individually, the corporate introduced a brand new contract with a “Fortune 500” airline for the event of latest electrical vertical takeoff and touchdown ((eVTOL)) plane batteries. That is an thrilling high-growth market phase the place the implementation of high-performance battery design and thermal security is of course essential. The understanding is that this explicit buyer would possible require a number of extra orders because the eVTOL market takes off.

Lastly, the newest replace is a $500k preliminary deployment order from a number one “Department of Defense contractor” with future issues of a multi-million greenback relationship over the following yr. This case highlights the appliance associated to drone and autonomous applied sciences that incorporate batteries requiring thermal safety.

Placing all of it collectively, the takeaway right here is for a stronger prime line over the following few quarters as these kind of engagements change into acknowledged. Administration touched on this outlook through the earnings conference call:

We imagine that we’re at an inflection level of KULR’s progress path. Prior to now yr, we have now made vital investments throughout analysis and improvement, facility infrastructure, SG&A and assembling in excessive caliber workforce. These strategic investments have resulted within the construct out of our holistic complete battery security platform, offering clients with an in depth set of options to realize battery sustainability inside their respective ecosystems…

Within the buyer engagements that we’re engaged on very intently, we count on the quantity to ramp of their enterprise in second half of 2022 and likewise nicely into 2023.

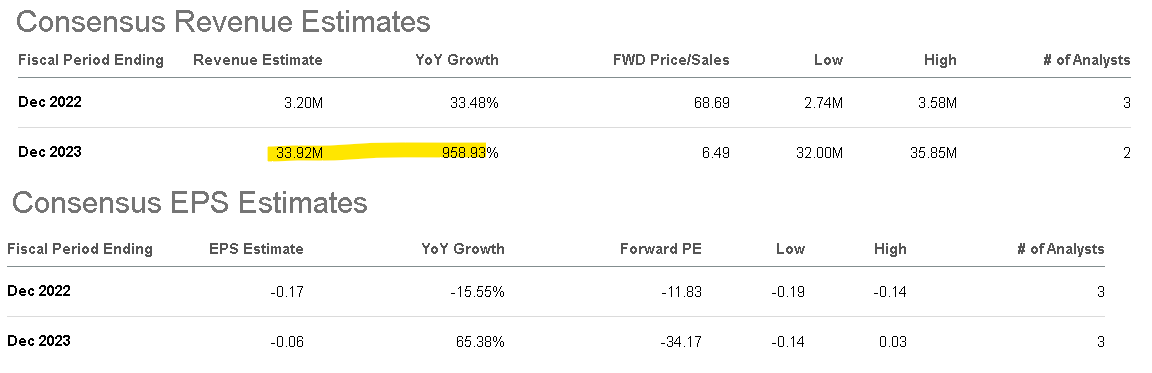

When it comes to valuations, there’s not a lot to go on with restricted targets and a scarcity of steerage from administration. We all know the corporate generated roughly $2.2 million in income over the previous yr, set to climb towards $3.2 million in 2022. By this measure, KULR is buying and selling at a ahead gross sales a number of of 69x.

Extra favorable is the outlook for 2023 the place a ramp-up within the commercialization technique can drive income close to $34 million throughout the present consensus throughout two Wall Road estimates indicative of the expansion inflection level. There’s loads of uncertainty with this determine, but when KULR can get wherever close to that quantity with a push over the following few quarters, we have now a stable progress inventory by any measure.

Searching for Alpha

KULR Inventory Worth Forecast

We fee KULR as a maintain forward of the corporate’s upcoming Q3 earnings report scheduled to be launched on November ninth. The report will even give administration a possibility to cowl the newest updates.

The excellent news for KULR is that shares have staged a formidable rally over the previous month, practically doubling from its October low when it traded down at $1.06. With a present market cap of round $200 million, the expectation right here is for this sort of excessive buying and selling swing to replicate the inventory’s speculative profile. So long as the inventory holds the ~$1.60 of assist, shares ought to keep some bullish momentum.

Searching for Alpha

The bullish case is that the market adoption of KULR Applied sciences merchandise accelerates with bigger orders and an increasing buyer base translating to a firming earnings outlook. Monitoring factors right here embody the gross margin and the common string of company developments detailing new contracts.

However, the elemental weak point goes again to the money move developments. If liquidity turns into a priority, bigger share issuances can be required for funding and dilutive to current shareholders. Some degree of a rising excellent share rely can be tolerated if it is supportive of increasing progress. 2023 can be essential on this regard. Buyers must see this as a long-term story which will take a few years to play out.

[ad_2]

Source link