[ad_1]

On the very least we want international trade to pay for importing crude oil, the lifeline of transport and logistics. We’re additionally import-dependent for quite a lot of objects, together with vaccine provides, metal and auto parts. Is there a draw back to having a big battle chest of {dollars}? It’s sophisticated, however sure, there are downsides. First, some excellent news although.

Signal of sound economic system

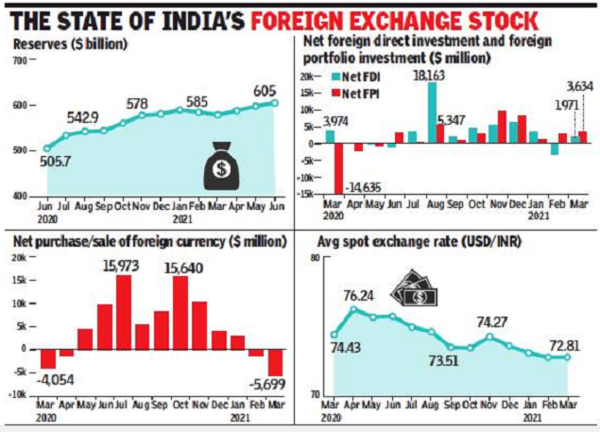

Not like all the most important, greenback hoarding central banks – China, Russia, Saudi Arabia and Japan – we’re not an export surplus nation. A lot of their pile is the buildup from years of incomes extra {dollars} than they spend. For us, it’s the reverse. We will be the solely massive Asian nation with a present account deficit, i.e., we import way more than we export, and nonetheless have massive international trade reserves. That’s creditable.

If yearly we fall wanting {dollars}, how come our foreign exchange inventory retains rising? The reason being the present account deficit is offset by a big inflow of capital flows. {Dollars} circulate into India via international portfolio traders (FPI) or as international direct funding (FDI). This influx from the acquisition of property like shares reveals the boldness of international traders in India’s progress prospects.

Prior to now three a long time, India has attracted practically $500 billion as FDI. Past FPI and FDI inflows into the inventory market are loans. These are referred to as exterior business borrowings. The overall excellent international loans are $560 billion, or about 93% of our international trade reserves. That’s a draw back.

Fickle associates

The inventory market inflows, particularly FPI, can simply and abruptly make an about-turn. Such traders could be fickle, or nervous, or just riskaverse, and can pull out funds on the drop of a hat, though pulling out FDI shouldn’t be that straightforward. Equally, Indian firms having massive greenback obligations of short- and long-term loans are additionally a warning signal. We’d like sufficient {dollars} to a minimum of repay the short-term money owed.

Even NRIs can withdraw massive greenback deposits abruptly. That’s what they did in 1990 when there was panic earlier than the primary Iraq battle. Additionally, if India’s ranking drops beneath funding grade, no international lender could be keen to refinance our previous loans. Our coffers will develop into empty repaying loans. That’s why India’s massive foreign exchange inventory, to the extent it has fickle flows, shouldn’t make us complacent. Until our exports exceed imports, we’ll stay weak.

Idle cash rocks the rupee

The second draw back to a big greenback pile is that it earns little or no curiosity. If it represents a nationwide asset, is there a greater use for it? Third, massive international holdings in India’s inventory market make its worth weak to ebbs and flows of foreign exchange. Certainly, the rupee often will get stronger on days when the inventory market rises, and vice versa. Is it wholesome that the buying energy of our importers relies on fickle international traders?

‘Free cash’ habit

The fourth draw back is that a big foreign exchange pile means RBI’s steadiness sheet will get bloated. For the reason that steadiness sheet is measured in rupees, it expands every time the rupee weakens. That is “free” achieve to RBI, which it will probably then cross on as dividends to the Centre. A really massive steadiness sheet dimension means even a slight weakening interprets into “notional” positive factors of 1000’s of crores, or revenue for RBI.

When foreign money fluctuates, the positive factors and losses ought to usually not be encashed. However massive revaluation positive factors on rupee weakening might develop into a seamless supply of fiscal financing for a central authorities in determined want. This could result in fiscal “habit” and even dilution of RBI’s independence.

Look past US greenback

The greenback shouldn’t be our foreign money. An excessive amount of of it will probably develop into a headache. Not like rupee debt we can not forgive our greenback debt. International locations like Russia, regardless of having massive international reserves, are transferring away from the greenback. There are geopolitical tensions with the US, and Russia doesn’t wish to rely on New York clearing banks (greenback transactions can solely be cleared by US banks). India also needs to look to diversify its foreign exchange holding away from the greenback, and look at the optimum dimension of international reserves for our wants.

!(operate(f, b, e, v, n, t, s) {

window.TimesApps = window.TimesApps || {};

const { TimesApps } = window;

TimesApps.loadFBEvents = operate() {

(operate(f, b, e, v, n, t, s) {

if (f.fbq) return;

n = f.fbq = operate() {

n.callMethod ? n.callMethod(…arguments) : n.queue.push(arguments);

};

if (!f._fbq) f._fbq = n;

n.push = n;

n.loaded = !0;

n.model = ‘2.0’;

n.queue = [];

t = b.createElement(e);

t.async = !0;

t.src = v;

s = b.getElementsByTagName(e)[0];

s.parentNode.insertBefore(t, s);

})(f, b, e, v, n, t, s);

fbq(‘init’, ‘593671331875494’);

fbq(‘observe’, ‘PageView’);

};

})(

window,

doc,

‘script’,

‘https://join.fb.internet/en_US/fbevents.js’,

);if(typeof window !== ‘undefined’) {

window.TimesApps = window.TimesApps || {};

const { TimesApps } = window;

TimesApps.loadScriptsOnceAdsReady = () => {

var scripts = [‘https://static.clmbtech.com/ad/commons/js/2658/toi/colombia_v2.js’,

‘https://www.googletagmanager.com/gtag/js?id=AW-877820074’,

‘https://imasdk.googleapis.com/js/sdkloader/ima3.js’,

‘https://tvid.in/sdk/loader.js’,

‘https://timesofindia.indiatimes.com/video_comscore_api/version-3.cms’,

‘https://timesofindia.indiatimes.com/grxpushnotification_js/minify-1,version-1.cms’,

‘https://connect.facebook.net/en_US/sdk.js#version=v10.0&xfbml=true’,

‘https://timesofindia.indiatimes.com/locateservice_js/minify-1,version-12.cms’

];

scripts.forEach(operate(url) {

let script = doc.createElement(‘script’);

script.sort=”textual content/javascript”;

if(!false && !false && url.indexOf(‘colombia_v2’)!== -1){

script.src = url;

} else if (!false && !false && url.indexOf(‘sdkloader’)!== -1) {

script.src = url;

} else if (url.indexOf(‘colombia_v2’)== -1 && url.indexOf(‘sdkloader’)== -1){

script.src = url;

}

script.async = true;

doc.physique.appendChild(script);

});

}

}

[ad_2]

Supply hyperlink